Useful Links and Info

European Parliament In-Depth Analysis, PE 759.348 (report on Construction and Renovation in the EU Housing Markets):

September 2025

Key points:

35 million buildings targeted for renovation by 2030 under the EU Renovation Wave.

60 million heat pumps to be installed by 2030.

Current renovation rate: ~1% per year (deep renovations only 0.2%) vs. ~2% needed to meet targets.

129 million outdated boilers currently installed across the EU, more than half inefficient.

This represents one of the largest structural retrofit programs globally.

Most Attractive Investment Segment

Worst-performing buildings (low energy efficiency classes, e.g., D–G) offer the strongest economics.

Why?

Higher upfront CAPEX, but

Significantly larger energy savings

Superior cost–benefit ratio vs. mid-efficiency assets

Higher valuation uplift post-renovation

Alignment with regulatory priority (EU focus on poorest-performing stock)

This creates a compelling value-add renovation strategy:

Acquire energy-inefficient assets → Standardized retrofit → Heating system upgrade (heat pumps) → Long-term rental stabilization.

Strategic Tailwinds

Regulatory push toward minimum energy standards

Carbon pricing revenues increasingly used for renovation subsidies

Structural housing undersupply across urban EU markets

Energy poverty affecting up to 8–16% of EU population, strengthening political support

EU BESS

EU Commission approves €279 million Czech State aid scheme to support investments in energy storage to foster the transition to a net-zero economy (2025)

Key points:

Targeting at least 1.5Mwh BESS of utility scale for CZ in a shape of direct grants.

Eu Battery Storage Report 2025

Key points:

EU Context

27.1 GWh installed in the EU in 2025 (+45% YoY)

77.3 GWh total EU installed capacity

Utility-scale = 55% of all new installations (15 GWh in 2025)

EU industry target: ~750 GWh by 2030 (10x growth required)

Battery storage has shifted from residential-driven growth to grid-scale infrastructure.

Market Signals Relevant for Czech Republic

Rising Price Volatility

Negative power prices in EU: 3.4% of the year in 2025 (~310 hours)

In leading markets (DE, NL, ES): >540 hours/year

Higher volatility = stronger arbitrage case for 1–4h BESS systems.

Czechia, as a highly interconnected Central European market, is exposed to the same cross-border volatility dynamics.

Revenue Model Reality

Successful EU markets show that IRR depends on:

Energy arbitrage (day-ahead / intraday spreads)

Frequency response

Ancillary services

Capacity mechanisms

Revenue stacking

Where stacking is allowed (e.g., Germany, UK), deployment scales quickly.

What Makes a Market Bankable (EU Evidence)

Top markets share:

No double grid charging

Priority grid access for storage

Clear ancillary market access

Streamlined permitting

Where these are missing, growth stagnates.

Czech Republic – Investment Implication

Czechia is not yet a top-5 EU market, meaning:

Early-stage grid-scale opportunity

Lower saturation risk vs Germany or Italy

Potential first-mover advantage

However, investment case depends on:

Access to ancillary service markets (ČEPS)

Grid connection timelines

Tariff treatment of storage (no double charging)

Possibility of revenue stacking

Strategic Takeaway

EU data confirms:

Utility-scale BESS is now the dominant growth segment (55%)

Price volatility is structurally increasing

Flexibility demand will surge as solar expansion continues

EU Energy Storage Targets by 2030 and 2050

Massive Structural Capacity Requirement

≥600 GW required by 2050 to support a fully decarbonised system.

Required deployment pace: ≥14 GW per year this decade.

Power storage is system-critical infrastructure.

Exponential Growth Gap = Investment Opportunity

Current deployment rates are far below required levels.

Europe had only ~3.8 GW of battery storage installed (at time of baseline reference in report).

Existing storage (~60 GW) is mostly pumped hydro (~57 GW), not batteries.

Implication: Battery storage must scale multiple times over to close the gap — creating long-term buildout visibility.

Duration Demand Evolves with Renewable Penetration

Up to ~60% variable renewables (vRES): demand is mainly short-duration storage (<10h).

Beyond ~60% vRES: need shifts toward daily and multi-day storage.

Implication:

In the 2025–2035 window, 1–4h / 2–6h BESS remains the core commercial segment.

Long-duration storage becomes more strategic post-2035.

The report confirms that EU storage deployment must accelerate dramatically to meet 2030 and 2050 targets.

This creates:

Long-term policy backing

Structural demand growth

Increasing monetisation of flexibility

A multi-decade infrastructure buildout cycle

Storage in Europe is transitioning from an opportunistic market to a core regulated energy infrastructure asset class..

Why now?

Both, from the point of energy market and construction market, there is a unique situation for growth.

Energy markets across Europe are undergoing structural change:

• Energy price volatility has accelerated decentralization.

• Grid operators increasingly require distributed flexibility and storage.

• Residential electrification is scaling rapidly.

• Govnt supports energy efficiency and storage deployment.

• Digital aggregation enables coordination of thousands of distributed assets.

As for the reconstruction point of view,

EU requires actively the renovation of thousands of homes annually, allowing a long-term work.

500k+

years of

work ahead

houses require

renovation in CZ

10+

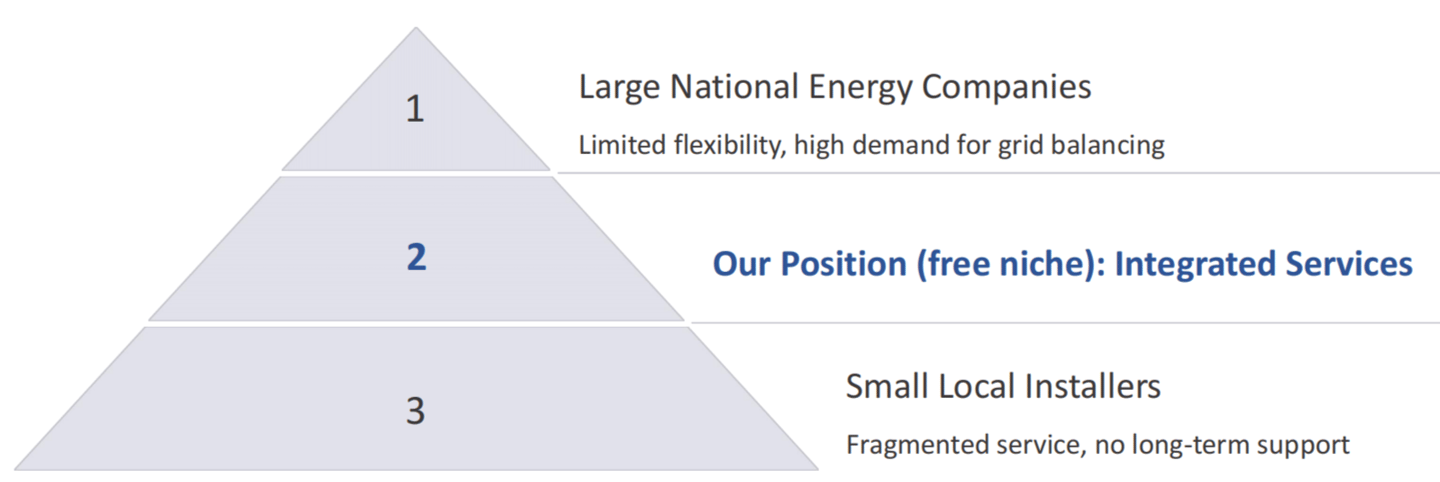

Market Context: EaaS in CZ

The European Energy-as-a-Service market presents a significant opportunity between two occupied segments.

We bridge the gap between large national enterprises lacking personalised service and small installers unable to provide comprehensive solutions or long-term warranty.

Customers' major pain points are:

excessively high energy prices, and a lack of options (from national firms);

absence of reliable services and guarantees (from local installers, as they often vanish from the market);

too many parties involved in the customer's home renovation (banks, architects, sellers, installers, etc).

AEM positioned as EaaS offering flexible tariffs, extended warranty, and a wide range of services.

© 2026. All rights reserved.